Understanding the effect of debits and credits in accounts is crucial for anyone involved in finance or accounting. Have you ever wondered how these fundamental concepts impact your financial statements? Whether you’re a business owner, student, or just curious about accounting, grasping these principles can empower you to make informed decisions.

Understanding Debits and Credits

Debits and credits form the backbone of accounting. Grasping these concepts is crucial for interpreting financial statements accurately.

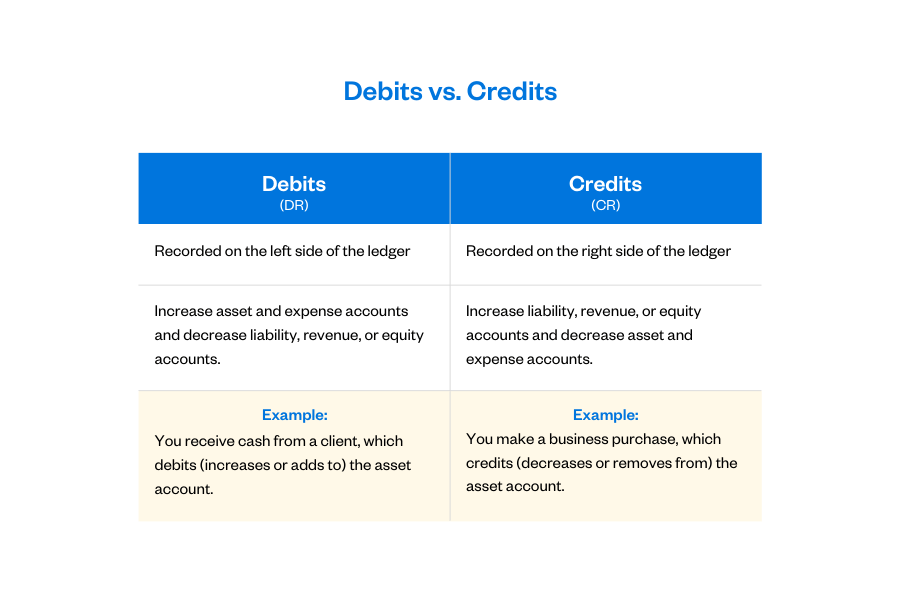

Definition of Debits

Debits signify an increase in assets or expenses. When you purchase inventory, for example, the inventory account increases, recording a debit. Another instance occurs when you pay rent; this also results in a debit to your expense account. In double-entry accounting, every debit must have a corresponding credit to maintain balance.

Definition of Credits

Credits indicate an increase in liabilities or equity. For instance, if you take out a loan, the cash account receives a credit because it represents borrowed funds. Similarly, when revenue is earned from sales, you credit the sales revenue account. Just like debits, credits need corresponding debits to ensure your accounts remain balanced.

The Accounting Equation

The accounting equation forms the foundation of double-entry bookkeeping. It states that Assets = Liabilities + Equity. Understanding this equation is vital for grasping how debits and credits impact your financial statements.

Assets, Liabilities, and Equity

Assets represent what you own, such as cash, inventory, or property. For instance:

- Cash: Money in your bank account.

- Inventory: Goods available for sale.

- Equipment: Tools used for business operations.

Liabilities signify what you owe. Examples include:

- Loans Payable: Money borrowed from banks.

- Accounts Payable: Bills owed to suppliers.

Equity reflects the owner’s interest in the business. This includes:

- Owner’s Capital: Initial investment made by the owner.

- Retained Earnings: Profits reinvested into the business.

Impact of Debits and Credits on the Equation

Debits increase assets or expenses while decreasing liabilities or equity. Conversely, credits boost liabilities or equity but decrease assets or expenses. Here’s how it works:

- When you buy equipment (asset):

- Debit Equipment (increases asset)

- Credit Cash (decreases asset)

- When you take out a loan:

- Debit Cash (increases asset)

- Credit Loans Payable (increases liability)

- When you earn revenue:

- Debit Accounts Receivable (increases asset)

- Credit Revenue (increases equity)

Each transaction maintains balance within the accounting equation, ensuring your financial picture remains clear and accurate.

Correct Statements About Debits and Credits

Understanding debits and credits is crucial for effective financial management. These concepts form the backbone of accounting, impacting how transactions are recorded and interpreted.

Statement Analysis

Debits increase assets or expenses, while credits increase liabilities or equity. For example, when you purchase office supplies with cash, you debit the supplies account to reflect the asset increase and credit the cash account to show a decrease in assets. Similarly, if your business takes a loan, it debits cash to reflect funds received and credits loans payable as an obligation.

Common Misconceptions

Many assume that debits always signify losses or costs; however, that’s incorrect. In reality, debits can represent valuable assets too. For instance:

- Purchasing equipment increases your asset base.

- Paying salaries reflects an expense but also supports employee productivity.

Additionally, some think credits only relate to income. While they do impact revenue accounts positively, credits also apply to liabilities, such as increasing accounts payable when receiving goods on credit. Understanding these nuances ensures accurate financial record-keeping.

Practical Applications in Accounting

Understanding the practical applications of debits and credits enhances your grasp of financial transactions. These concepts play a vital role in accurately recording and interpreting business activities.

Examples of Debits and Credits

Debits and credits work together in various scenarios. Here are some clear examples:

- Purchasing Inventory: When you buy inventory worth $5,000, you debit the Inventory account (increasing assets) and credit Cash or Accounts Payable (decreasing cash or increasing liabilities).

- Receiving Payment from Customers: If a customer pays $1,200 for services rendered, you debit Cash (increasing assets) and credit Revenue (increasing equity).

- Taking Out a Loan: When obtaining a loan for $10,000, you debit Cash (increasing assets) while crediting Loans Payable (increasing liabilities).

These instances illustrate how each transaction maintains balance within your accounts.

Importance in Financial Reporting

Debits and credits are foundational to accurate financial reporting. They ensure that every transaction reflects true economic activity. Here’s why they matter:

- Balance Sheet Accuracy: Properly recording debits and credits guarantees that your balance sheet remains balanced—assets equal liabilities plus equity.

- Income Statement Clarity: Accurate entries help depict revenues and expenses correctly on your income statement, leading to better performance insights.

- Regulatory Compliance: Adhering to these principles supports compliance with accounting standards like GAAP or IFRS.

Understanding their significance empowers effective decision-making based on reliable data.