Starting a new business is an exciting journey, but it comes with its fair share of challenges. One of the most pressing concerns for any entrepreneur is understanding potential legal liabilities. Two related entities that can help the new business owner foresee potential legal liabilities are attorneys and insurance providers. These professionals play crucial roles in safeguarding your venture from unexpected pitfalls.

Understanding Legal Liabilities for New Business Owners

New business owners face various legal liabilities, making it essential to identify potential risks. Attorneys play a crucial role in navigating these complexities. They offer guidance on regulatory compliance and contract reviews. For example, an attorney can help you draft employee contracts that minimize the risk of disputes.

Another important entity is insurance providers. Insurance helps protect your business from unexpected claims. Liability insurance covers incidents like customer injuries on your property or product defects. For instance, if a customer slips and falls in your store, liability coverage can shield you from financial loss.

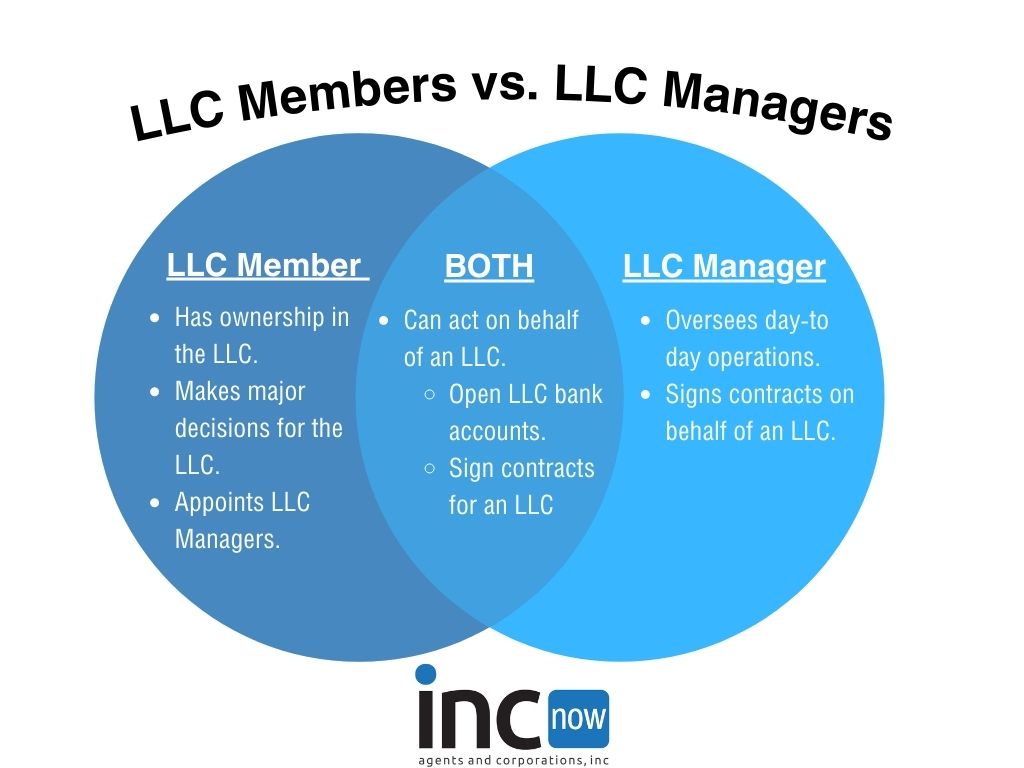

When considering legal structures, think about how they affect liability exposure. Choosing between sole proprietorships and LLCs impacts personal liability. An LLC generally protects your personal assets from business debts.

In addition to these entities, staying informed about local laws is vital. Your local chamber of commerce often provides resources for new businesses. They may offer workshops on legal responsibilities or access to experts who specialize in small business law.

To summarize, engaging with attorneys and insurance providers significantly aids in understanding and mitigating potential legal liabilities.

Importance of Legal Preparedness

Legal preparedness plays a crucial role in the success and longevity of your business. Understanding potential legal liabilities helps you navigate challenges and protect your venture from unexpected issues.

Key Reasons to Anticipate Liabilities

Anticipating liabilities offers several advantages:

- Protects assets: Identifying risks helps safeguard personal and business assets from claims.

- Enhances decision-making: Knowing legal obligations improves strategic planning and operational choices.

- Increases credibility: Demonstrating awareness of legal responsibilities builds trust with customers, partners, and investors.

Addressing these factors proactively strengthens your position in the market.

Benefits of Early Intervention

Early intervention can significantly reduce the impact of legal issues. Here are some benefits:

- Cost savings: Tackling potential problems early often results in lower expenses than dealing with crises later.

- Minimizes disruptions: Proactive measures can prevent interruptions that affect productivity or reputation.

- Improves compliance: Regularly reviewing contracts and regulations keeps your business aligned with current laws.

By prioritizing legal preparedness, you enhance resilience against unforeseen challenges.

Two Related Entities That Can Help

Understanding potential legal liabilities is crucial for new business owners. Two key entities that provide support are business consultants and attorneys.

Entity One: Business Consultants

Business consultants offer valuable insights to help you navigate the complexities of starting and running a business. They analyze your operations, identify risks, and recommend strategies to mitigate them. For instance, they may assist in:

- Creating a solid business plan to outline goals and compliance requirements.

- Conducting market research to understand industry standards and regulations.

- Developing risk management strategies tailored to your specific sector.

By collaborating with a consultant, you’re better equipped to foresee challenges before they impact your venture.

Entity Two: Attorneys

Attorneys play an essential role in safeguarding your business against legal issues. They provide expertise on various aspects of law that affect entrepreneurs. Their services typically include:

- Advising on business structure, helping you choose between sole proprietorships or LLCs based on liability exposure.

- Reviewing contracts for clarity and compliance, which prevents misunderstandings with clients or suppliers.

- Ensuring regulatory adherence, keeping you informed about local laws that could affect operations.

Utilizing an attorney’s knowledge strengthens your ability to handle potential liabilities effectively.

Entity Two: Legal Advisors

Legal advisors play a crucial role in helping new business owners navigate potential legal liabilities. By offering specialized knowledge, they help you understand the complexities of business law and how it applies to your venture.

Expertise of Legal Advisors in Risk Management

Legal advisors provide expertise that is essential for risk management. They analyze contracts, ensuring compliance with local regulations and identifying potential pitfalls. For instance, a legal advisor can spot vague clauses that may lead to disputes later on. Additionally, they can guide you through regulatory requirements specific to your industry, reducing the likelihood of fines or penalties. Their insights into liability issues—such as employee relations or product safety—can save significant costs down the line.

How to Choose the Right Legal Advisor

Choosing the right legal advisor requires careful consideration. First, assess their experience in your particular industry; this ensures they’re familiar with relevant laws and challenges. Second, evaluate their communication style; effective communication fosters a better working relationship. Third, check references or reviews from other clients to gauge their reliability and effectiveness. Finally, consider whether they offer services tailored to small businesses; some firms specialize in startups and can provide customized support based on your unique needs.

By understanding these aspects of legal advisors’ roles and selecting one who aligns with your goals, you set yourself up for greater success while minimizing risks associated with running a business.

Best Practices for New Business Owners

New business owners can take proactive steps to mitigate potential legal liabilities. By following best practices, you can create a stronger foundation for your venture.

Creating a Comprehensive Business Plan

A comprehensive business plan serves as a roadmap for your business. It outlines objectives and strategies while identifying potential risks. Include sections that address:

- Market analysis: Understand your target audience and competitors.

- Financial projections: Estimate revenues, expenses, and funding needs.

- Operational plans: Detail daily operations and risk management strategies.

By having these elements in place, you anticipate challenges and develop effective solutions before they arise.

Regular Review of Legal Obligations

Regularly reviewing legal obligations keeps you compliant with relevant laws. You should focus on:

- Employment laws: Ensure proper employee classification and fair labor practices.

- Tax requirements: Stay updated on local, state, and federal tax regulations.

- Licenses and permits: Confirm that all necessary licenses are active.

By actively managing these responsibilities, you reduce the likelihood of facing penalties or legal disputes down the line.