Are you looking to maximize your financial potential? Understanding how income-shifting and timing strategies are examples of effective wealth management techniques can be a game changer. These strategies allow you to optimize your earnings, reduce tax liabilities, and ultimately enhance your overall financial health.

Overview of Income-Shifting and Timing Strategies

Income-shifting and timing strategies serve as powerful tools for optimizing your financial situation. These techniques focus on reallocating income to minimize tax liabilities while maximizing earnings. Here are some examples that illustrate their effectiveness:

- Shifting income to lower tax brackets: You can transfer certain income sources, like rental properties or business profits, to family members in lower tax brackets. This approach may reduce the overall tax burden.

- Utilizing retirement accounts: Contributing to a 401(k) or IRA allows you to defer taxes until withdrawal age. You gain immediate tax benefits while saving for retirement, which enhances long-term financial health.

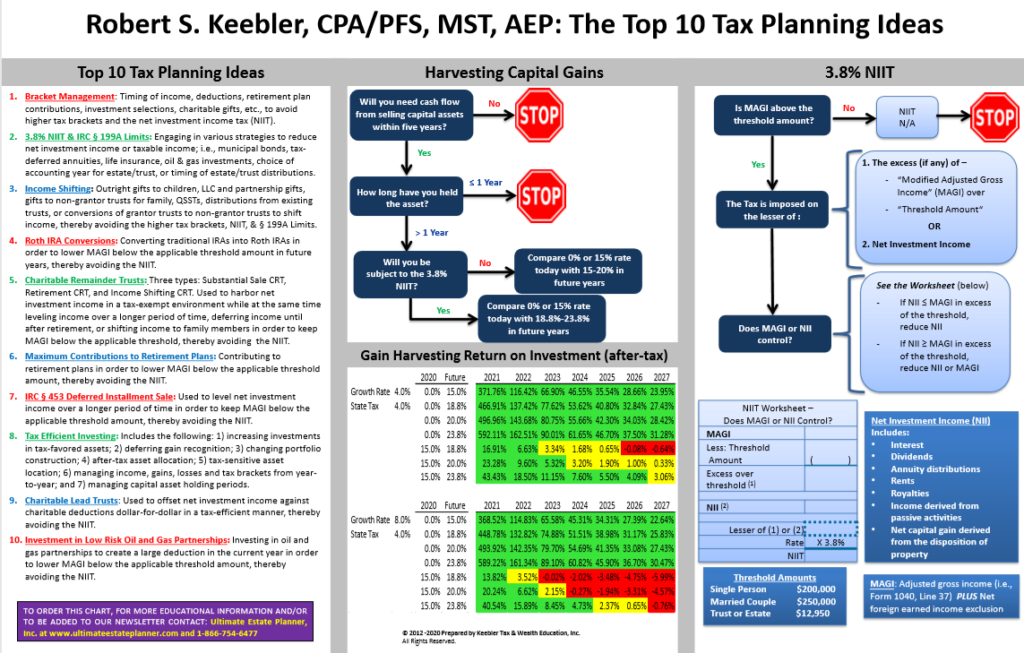

- Timing capital gains: By holding investments for over a year before selling, you qualify for long-term capital gains rates, which are typically lower than short-term rates. This strategy maximizes your investment returns.

- Deferring bonuses: If possible, negotiate with your employer to delay bonus payments until the following year. Doing so may keep you within a lower tax bracket during the current year.

- Leveraging deductions: Bunching itemized deductions into one year can increase your total deduction amount. For instance, consider prepaying property taxes or making charitable contributions in one lump sum.

These strategies highlight practical ways individuals can enhance their wealth through informed decision-making and strategic planning.

Types of Income-Shifting Strategies

Income-shifting strategies enhance your financial position by reallocating or timing income effectively. Below are key methods that illustrate how you can implement these strategies.

Tax Avoidance Techniques

Tax avoidance techniques provide legal ways to minimize tax liabilities. For instance, shifting income to family members in lower tax brackets reduces overall taxable income. You might also consider utilizing Health Savings Accounts (HSAs) for medical expenses, which allow pre-tax contributions. Additionally, contributing to a traditional IRA defers taxes until withdrawal, lowering your current taxable income.

- Gift Tax Exemptions: Giving gifts up to $17,000 annually per recipient avoids gift taxes.

- 529 Plans: Investing in education savings accounts offers tax-free growth if used for qualified education expenses.

- Charitable Contributions: Donating to charities provides deductions that reduce your taxable income while supporting causes you care about.

Wealth Distribution Methods

Wealth distribution methods focus on optimizing the flow of assets among family members. For example, using trusts can help you transfer assets while minimizing estate taxes. Establishing a family limited partnership allows for shifting control and ownership of business interests while keeping assets within the family.

- Income Splitting: Spreading income among various family members helps take advantage of lower tax rates.

- Retirement Account Rollovers: Rolling over funds from one retirement account to another delays taxation and maintains wealth accumulation.

- Capital Gains Timing: Selling investments during years with lower total income minimizes capital gains taxes.

These strategies demonstrate effective ways to manage financial resources strategically.

Timing Strategies in Income Management

Timing strategies play a crucial role in managing income effectively. These methods can significantly impact your financial outcomes by maximizing earnings and minimizing tax liabilities.

Short-Term Timing Strategies

Short-term timing strategies involve immediate actions that influence your income and taxes within the current year. Here are some effective examples:

- Deferring Bonuses: If your employer offers bonuses, consider deferring them to the next tax year. This approach may help you stay within a lower tax bracket for the current year.

- Timing Capital Gains: Selling investments at specific times can minimize taxes. For instance, if you expect higher capital gains tax rates next year, selling this year could result in savings.

- Accelerating Deductions: You might choose to pay deductible expenses early. For example, prepaying state taxes or medical bills before year’s end allows you to claim these deductions sooner.

Long-Term Timing Strategies

Long-term timing strategies focus on decisions affecting income over multiple years. Implement these practices for optimal results:

- Utilizing Retirement Accounts: Contributing to accounts like 401(k)s or IRAs allows for tax-deferred growth over time. The earlier you start contributing, the more significant your potential growth.

- Implementing Tax-Loss Harvesting: This strategy involves selling losing investments to offset gains from winning ones over several years. By balancing gains and losses strategically, you can reduce taxable income.

- Planning Withdrawals Strategically: For retirees, withdrawing funds from retirement accounts during lower-income years minimizes taxation on those withdrawals.

Adopting these timing strategies enhances your ability to manage income effectively while navigating complex financial landscapes successfully.

Benefits of Using These Strategies

Using income-shifting and timing strategies offers several key benefits that can enhance your financial situation.

Maximizing tax efficiency is a primary advantage. By shifting income to family members in lower tax brackets, you reduce the overall tax burden for your household. Additionally, utilizing retirement accounts allows you to defer taxes on earnings until withdrawal.

Improving cash flow management enhances liquidity. Timing capital gains strategically can help you minimize taxes during high-income years. Deferring bonuses further aids this by keeping you within a lower tax bracket when it matters most.

Deductions can be optimized for greater savings. Bunching deductions into one year maximizes their impact, ensuring that you’re taking full advantage of available credits and exemptions. This approach often results in substantial tax reductions.

These strategies not only help in minimizing taxes but also facilitate smarter wealth distribution among family members and beneficiaries. Trusts and family limited partnerships offer structured approaches to asset management, enabling better control over how assets are passed down through generations.

Incorporating these techniques into your financial planning encourages proactive decision-making about earnings and expenditures. You’ll find that the right application of income-shifting and timing strategies significantly boosts overall financial health while fostering long-term wealth growth.