Have you ever considered how your generosity can benefit not just those in need but also your own financial situation? One of the financial advantages of donating to charitable causes is that the donation can be tax-deductible. This means that when you contribute to a qualified charity, you might reduce your taxable income and potentially lower your overall tax bill.

Overview of Charitable Donations

Charitable donations offer significant financial advantages. One primary benefit is the potential for tax deductions. When you donate to a qualified charity, you can often deduct the amount from your taxable income, which lowers your overall tax bill.

For instance, if you donate $500 to a recognized nonprofit organization, this amount may reduce your taxable income by $500. As a result, if you’re in a 24% tax bracket, this deduction could save you $120 on your taxes.

Additionally, strong financial planning includes understanding how charitable contributions impact various aspects of your finances. Donating regularly can also help establish goodwill and enhance personal fulfillment.

Moreover, many employers match employee donations. This means that when you contribute to a charity, your employer might double or even triple that amount. It’s an effective way to maximize the impact of your generosity while enjoying tax benefits.

Consider these examples:

- Cash Donations: Direct monetary gifts to charities.

- Property Donations: Gifting items like clothing or vehicles.

- Volunteer Hours: Some organizations value volunteer time as a donation and may provide matching contributions based on hours worked.

Make sure to keep accurate records of all donations for proper documentation during tax season. Understanding these elements ensures that charitable giving aligns with both personal values and financial strategies.

Tax Deductions for Donors

Donating to charitable causes offers significant tax benefits. Donations made to qualified charities may qualify as tax-deductible, which can effectively lower your taxable income and reduce your overall tax burden.

Understanding Tax Deductions

Tax deductions are crucial in maximizing the financial impact of your donations. For instance, if you donate $500 to a qualified charity, you could save approximately $120 on taxes if you’re in a 24% tax bracket. This means that generous contributions not only support good causes but also provide tangible financial relief at tax time.

Eligibility Criteria

To ensure your donation qualifies for a deduction, adhere to specific eligibility criteria:

- Qualified Organizations: Your donation must go to an IRS-recognized 501(c)(3) organization.

- Documentation: Keep records of all donations. Receipts or bank statements should detail the amount and date.

- Limitations: Be aware of limits on deductions based on adjusted gross income (AGI). Generally, cash contributions are limited to 60% of AGI.

- Itemizing Deductions: You must itemize deductions on Schedule A instead of taking the standard deduction.

By understanding these factors, you can optimize your charitable contributions while reaping financial rewards come tax season.

Long-Term Financial Benefits

Donating to charitable causes offers significant long-term financial benefits. These advantages extend beyond immediate tax deductions, impacting your overall financial strategy.

Enhanced Tax Strategies

Tax deductions from charitable donations can optimize your tax situation. Contributions reduce your taxable income, potentially placing you in a lower tax bracket. For example, if you donate $1,000 and you’re in the 24% bracket, that donation may save you $240 on your taxes. Additionally, utilizing donor-advised funds allows for strategic giving over time while maximizing deductions in high-income years.

Impact on Estate Planning

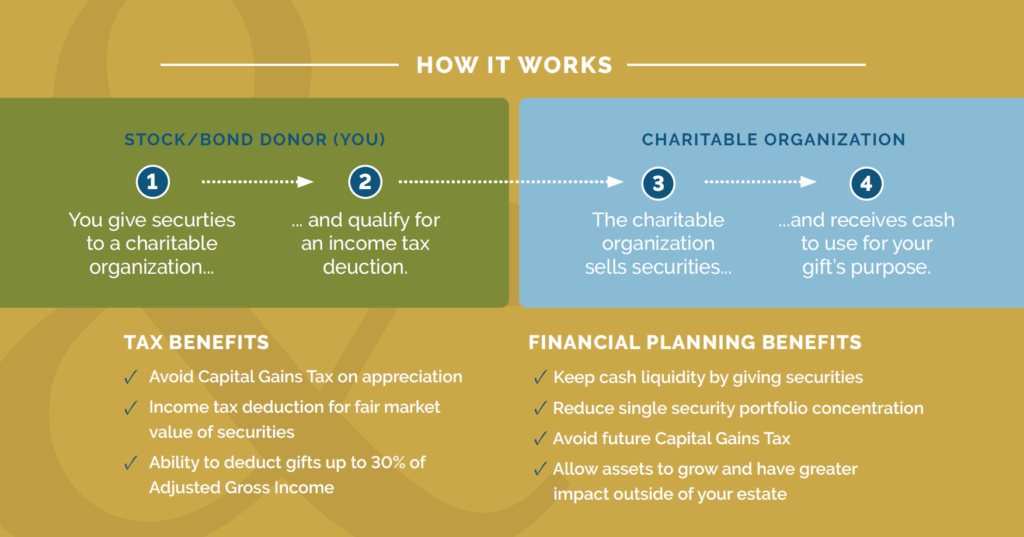

Charitable donations play a crucial role in estate planning. You can reduce the size of your taxable estate by leaving assets to charities instead of heirs. For instance, donating appreciated stocks avoids capital gains taxes while benefiting a cause you care about. Also, establishing a charitable remainder trust provides income during your lifetime and donates remaining assets to charity upon passing.

Engaging with these strategies not only supports meaningful causes but also enhances your financial health over time.

Personal Financial Well-being

Donating to charitable causes enhances your personal financial well-being. The tax advantages from these contributions can provide significant savings. Also, engaging in philanthropy fosters emotional rewards and strengthens community ties.

Emotional Rewards

Giving to charity often leads to feelings of happiness and satisfaction. Studies show that individuals who donate report higher levels of emotional well-being. It’s fulfilling to know your contribution supports a cause you care about. Many find joy in seeing the direct impact of their donations, whether it’s funding education or providing shelter for those in need.

Community Engagement

Your donations can strengthen community bonds and foster a sense of belonging. When you support local charities, you contribute to initiatives that improve your neighborhood. For instance, volunteering at food banks or donating school supplies helps create a more supportive environment for everyone. Additionally, participating in community events organized by these charities can enhance social networks and connections with like-minded individuals.