Imagine opening your balance sheet and seeing a mix of numbers that represent your financial life. Credit card bills, medical bills, car loans, and mortgages are all examples of liabilities that impact your overall financial health. Understanding these elements is crucial for managing your finances effectively.

Understanding On The Balance Sheet

On the balance sheet, financial liabilities play a crucial role in assessing your overall financial health. Credit card bills represent short-term debt that accrues interest if unpaid. Tracking these is vital to avoid unnecessary costs.

Medical bills often arise unexpectedly and can accumulate quickly. They impact your cash flow significantly, so understanding their timing and amounts helps manage finances effectively.

Car loans are another common liability. They typically come with fixed monthly payments over several years. Regularly reviewing this loan ensures you stay on top of your budget and future planning.

Mortgages usually comprise the largest debt for many individuals or families. These long-term loans require careful management due to their size and duration, making it essential to understand interest rates and payment schedules.

These examples highlight how various liabilities influence your financial situation. By monitoring each category closely, you maintain better control over your personal finances.

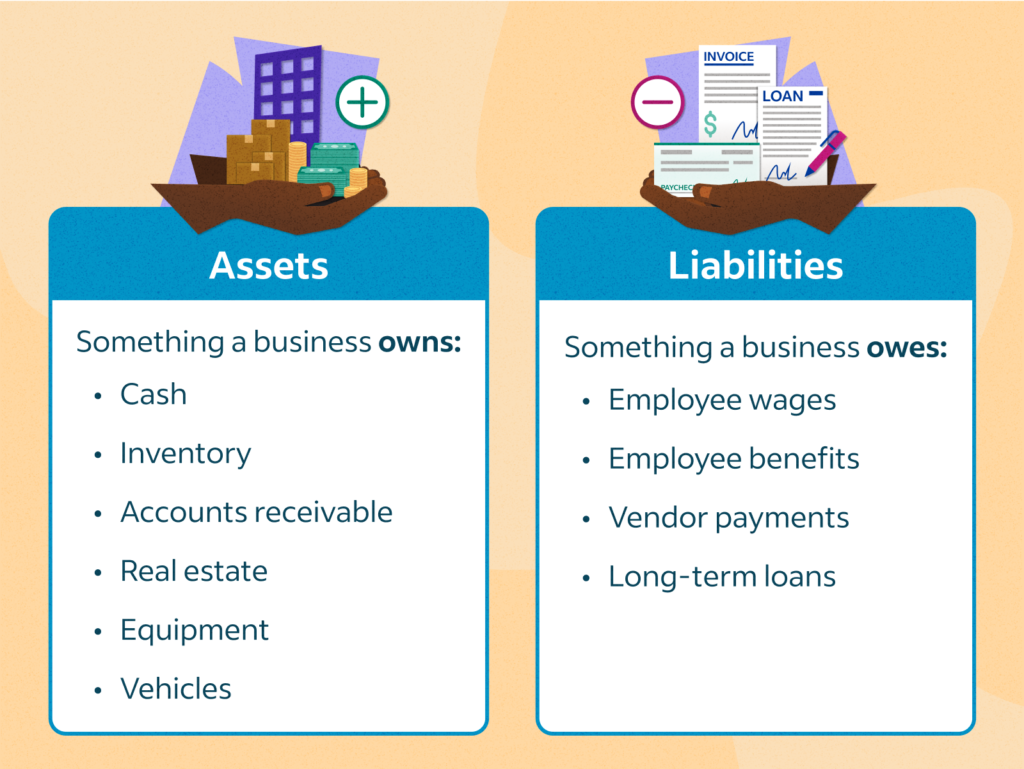

Types Of Liabilities

Understanding the different types of liabilities is essential for effective financial management. Each type impacts your overall financial health and requires careful monitoring.

Credit Card Bills

Credit card bills represent short-term debts that can accumulate quickly. When you carry a balance, interest accrues, increasing total debt. It’s vital to track these expenses monthly to avoid overspending. Regular payments help maintain a healthy credit score while minimizing interest costs.

Medical Bills

Medical bills often arise unexpectedly and can strain your cash flow. They may include doctor’s fees, hospital stays, or treatments not covered by insurance. Managing these bills involves negotiating payment plans or seeking assistance programs when necessary. Keeping records of medical expenses also aids in budgeting for future healthcare needs.

Car Loans

Car loans typically come with fixed monthly payments and set terms. These loans enable you to finance vehicle purchases without paying the full amount upfront. Stay on top of your payments to avoid repossession and damage to your credit score. Regularly reviewing loan statements helps ensure you’re adhering to the budget while considering refinancing options if rates drop.

Mortgages

Mortgages are often the largest debt individuals or families face. With long repayment periods, they require diligent management of payment schedules and interest rates. Understanding mortgage terms ensures you make informed decisions regarding refinancing or additional payments on principal amounts. Consistent monitoring of mortgage statements helps maintain control over this significant liability.

Impact On Financial Health

Financial liabilities like credit card bills, medical bills, car loans, and mortgages play a crucial role in determining your financial health. They influence cash flow, credit scores, and long-term wealth accumulation. Understanding these impacts helps you make informed decisions about managing your finances.

Short-Term Implications

Credit card bills can lead to immediate cash flow challenges if unpaid. You might find yourself juggling payments or relying on savings. Timely payments are essential to avoid high-interest charges that can add up quickly. Medical bills often arrive unexpectedly and can strain budgets, making it vital to negotiate manageable payment terms when necessary. Car loans present fixed monthly obligations that require consistent budgeting; missing payments may negatively affect your credit score.

Long-Term Consequences

Mortgages frequently represent the largest debt for individuals or families, impacting financial stability over time. A well-managed mortgage contributes positively to equity growth but mismanagement could lead to foreclosure. Accumulating too much debt from various sources may hinder future borrowing abilities and limit investment opportunities. Consider how each liability influences overall net worth; excessive liabilities diminish financial security as they accumulate interest over time.

Strategies For Managing Debt

Managing debt effectively requires a combination of strategies tailored to your financial situation. Here are some practical approaches:

- Create a Budget: You should outline all income and expenses. This helps identify areas where you can cut back, freeing up funds for debt repayment.

- Prioritize Payments: Focus on high-interest debts first, such as credit card bills. Paying these off reduces the total interest paid over time.

- Negotiate with Creditors: Contact your creditors to discuss payment plans or reductions in interest rates. Many are willing to work with you if you’re proactive.

- Consider Debt Consolidation: Look into consolidating multiple debts into one loan with a lower interest rate. This simplifies payments and may lower monthly obligations.

- Set Up an Emergency Fund: You should aim for at least three months’ worth of expenses saved. This prevents additional debt from unexpected costs like medical bills or car repairs.

- Use Automatic Payments: Automate bill payments to avoid late fees and missed payments, which can damage your credit score.

- Monitor Your Credit Report: Regularly check your credit report for errors or fraudulent activity that could impact your financial health.

- Educate Yourself About Financial Literacy: Knowledge is power when it comes to managing personal finances; consider taking courses or reading books about budgeting and investing.

Implementing these strategies can lead to better control over your financial health, helping you manage liabilities like car loans and mortgages more efficiently while fostering long-term wealth accumulation.