If you’re exploring financing options for your home, you might have come across the term non conforming loan. But what exactly does it mean? Unlike conventional loans that adhere to strict guidelines set by Fannie Mae and Freddie Mac, non conforming loans offer flexibility for borrowers who don’t fit the traditional mold.

These loans can be a game-changer if you’re self-employed or looking to buy a high-value property. They cater to unique financial situations that standard lenders often overlook. Are you curious about how these loans work and whether they might be right for you? This article dives into key examples of non conforming loans, their benefits, and what to consider before applying. By understanding this niche in the mortgage market, you’ll be better equipped to make informed decisions on your path to homeownership.

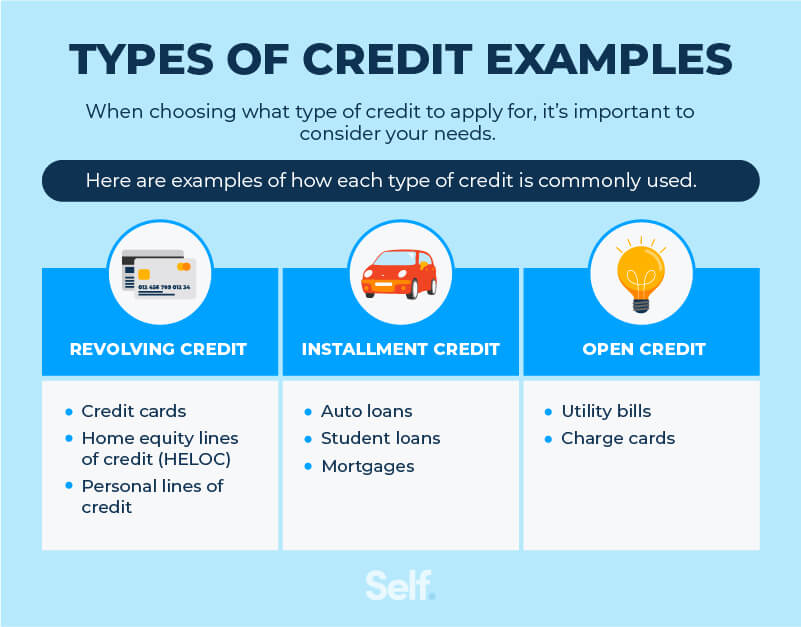

What Is a Non Conforming Loan?

A non conforming loan is a type of mortgage that doesn’t meet the guidelines set by Fannie Mae and Freddie Mac. These loans cater to borrowers with unique financial situations or those seeking larger amounts than conventional limits allow. Here are some examples:

- Jumbo Loans: Designed for properties priced above conforming loan limits, these loans provide financing for high-value homes. For instance, if you’re looking at a mansion in an expensive neighborhood, a jumbo loan may be your best option.

- Alt-A Loans: These loans target borrowers with good credit but limited documentation, such as self-employed individuals or freelancers. They offer flexible options without stringent income verification.

- Subprime Loans: Aimed at borrowers with lower credit scores who might struggle to get approved for conventional loans. While interest rates tend to be higher, they help individuals secure financing when traditional options fall short.

Non conforming loans serve various purposes and can significantly benefit specific groups of borrowers. Consider your financial situation to determine if one of these loans fits your needs.

Types of Non Conforming Loans

Non conforming loans include various types tailored to meet specific borrower needs. Understanding these types helps you choose the right financing option for your situation.

Jumbo Loans

Jumbo loans cater to buyers seeking properties that exceed the conforming loan limit. In 2025, this limit stands at $726,200 in most areas. However, it can be higher in high-cost regions. Jumbo loans typically offer competitive interest rates despite their larger amounts, which often range from $500,000 to several million dollars. These loans require strong credit profiles and substantial down payments—usually around 20%.

Alt-A Loans

Alt-A loans serve borrowers who have good credit but can’t provide full documentation. They bridge the gap between prime and subprime lending by offering more flexible terms than conventional loans. With Alt-A loans, lenders may consider factors like income verification through bank statements instead of W-2 forms. Borrowers might find loan amounts varying widely based on individual circumstances but generally fall within standard limits up to $1 million or more depending on the lender’s criteria.

While each type of non conforming loan has its unique characteristics and target audience, understanding them can significantly enhance your home financing options.

Advantages of Non Conforming Loans

Non conforming loans offer distinct benefits for borrowers who don’t fit traditional lending criteria. These advantages cater to a variety of financial situations.

Flexibility in Qualification

Flexibility is a major advantage of non conforming loans. Unlike conventional loans, these options accommodate various financial circumstances. For instance, self-employed individuals often struggle to provide the extensive documentation required by standard lenders. With non conforming loans, you can secure financing with less stringent requirements. Moreover, if your credit history has some blemishes or you’re a first-time buyer without an established credit score, these loans may still be accessible.

Potential for Higher Loan Amounts

The potential for higher loan amounts sets non conforming loans apart. Jumbo loans specifically allow financing beyond the typical limits set by Fannie Mae and Freddie Mac. This means if you’re eyeing a high-value property that exceeds $726,200 in most areas, you could qualify for significant funding through a jumbo loan. Additionally, since these loans aren’t subject to the same caps as conventional options, they cater well to luxury homebuyers looking for larger mortgages.

Disadvantages of Non Conforming Loans

Non conforming loans come with several drawbacks that borrowers should consider. While they offer flexibility, certain aspects can create challenges in the lending process.

Higher Interest Rates

Non conforming loans typically feature higher interest rates compared to conventional loans. Lenders often view these loans as riskier due to less stringent qualification standards. For example:

- Jumbo loans may charge 0.25% to 0.75% more than traditional mortgages.

- Alt-A and subprime loans also reflect increased interest rates based on creditworthiness.

These elevated rates can significantly increase your monthly payments and overall borrowing costs.

Stricter Loan Terms

You might encounter stricter loan terms with non conforming loans, which can affect your borrowing experience. Some key points include:

- Larger down payment requirements, often around 20% for jumbo loans.

- Shorter repayment periods, sometimes limiting options to 15 or 20 years instead of typical 30-year terms.

These factors could make it challenging for you to secure financing or afford the long-term commitment associated with these types of loans.