When it comes to managing your finances, understanding the difference between a line of credit vs credit card can save you both time and money. While they might seem similar at first glance, each option offers unique benefits that cater to different financial needs. Have you ever wondered which one is right for you?

Overview of Line of Credit and Credit Card

A line of credit provides a flexible borrowing option. It allows you to withdraw funds as needed, up to a predetermined limit. You only pay interest on the amount you draw, which can lower your overall costs compared to other forms of credit.

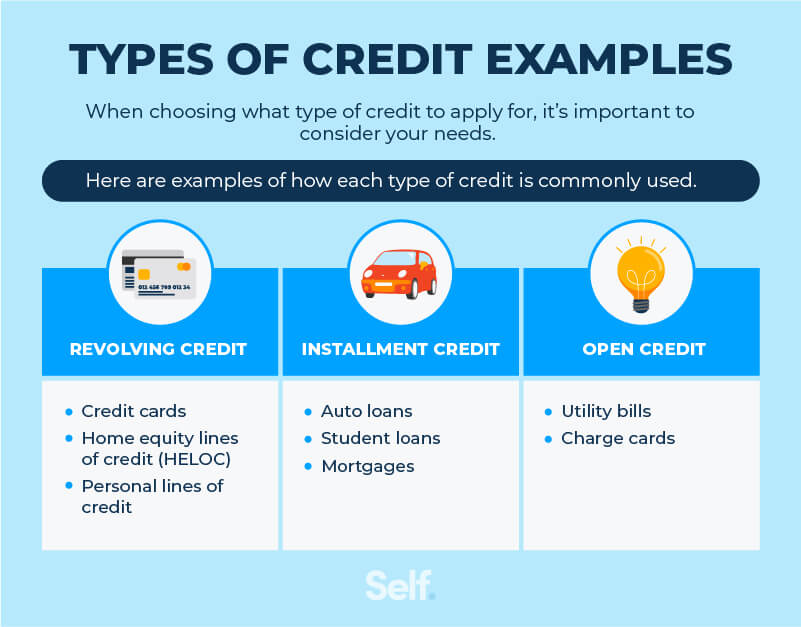

Conversely, a credit card offers a revolving line of credit that’s tied to your account. Each purchase reduces your available balance, but you can repay the amount in full or make minimum payments each month. If you carry a balance, interest accumulates on any unpaid amounts.

Both options serve different purposes. For instance:

- Line of Credit: Ideal for ongoing expenses like home repairs or education.

- Credit Card: Great for everyday purchases and building rewards through cashback or points.

When considering your financial needs, think about how often you’ll need access to funds and whether you prefer fixed monthly payments or flexibility in repayment terms. Would you rather keep track of multiple transactions with a credit card, or do you need the simplicity of drawing from one source?

Key Differences Between Line of Credit and Credit Card

Understanding the key differences between a line of credit and a credit card can help you make informed financial decisions. Each option offers unique features tailored to different needs.

Usage and Flexibility

A line of credit offers greater flexibility for accessing funds. You can withdraw any amount up to your limit whenever necessary, making it ideal for unexpected expenses like home repairs or medical bills. For instance, if you have a $10,000 line of credit, you might choose to borrow $2,000 one month and pay it back before borrowing another $3,500 later.

On the other hand, a credit card serves as a revolving account that’s perfect for daily purchases. When you use your credit card for groceries or gas, you’re essentially reducing your available balance but not withdrawing cash directly. If your limit is $5,000 and you spend $200 on groceries, you’ll be left with $4,800 until you make payments.

Interest Rates and Fees

Interest rates differ significantly between these two options. Generally speaking, lines of credit feature lower interest rates compared to most credit cards. For example:

- A typical line of credit may charge around 6% to 12% APR.

- Conversely, many credit cards charge 15% to 25% APR or even higher for unpaid balances.

Fees also vary; lines of credit often include annual fees or maintenance charges while many credit cards offer no annual fee options but could impose late payment penalties or foreign transaction fees instead.

Consider how each option aligns with your financial habits—whether it’s the flexible access offered by lines of credit or the convenience provided by using a credit card for everyday spending.

Benefits of a Line of Credit

A line of credit offers several key advantages that can greatly benefit your financial management. These benefits make it an appealing option for those needing flexible access to funds.

Access to Larger Amounts

Accessing larger amounts is one of the primary benefits of a line of credit. Many lines of credit allow you to borrow substantial sums, often ranging from $5,000 to $100,000 or more, depending on your creditworthiness and lender policies. This flexibility means you can handle significant expenses such as home renovations or medical bills without seeking multiple loans. You draw only what you need up to your limit, making it easier to manage cash flow.

Lower Interest Rates

Lower interest rates are another compelling advantage. Lines of credit typically come with interest rates between 6% and 12% APR, significantly lower than many credit cards, which often charge 15% to 25% APR or higher. This difference in rates can save you money if you’re borrowing larger amounts over time. Since you pay interest only on the amount drawn rather than the total limit, this option works well for those who plan their borrowing carefully.

Benefits of a Credit Card

Credit cards offer several benefits that enhance your financial flexibility and purchasing power. They provide convenience for everyday transactions, making it easy to manage expenses without carrying cash.

Rewards and Perks

Many credit cards include attractive rewards programs. For example:

- Cashback: Some cards return a percentage of your spending as cash back on purchases.

- Travel Points: Others allow you to earn points redeemable for flights or hotel stays.

- Sign-Up Bonuses: Many issuers offer substantial bonuses when you meet initial spending thresholds.

These rewards can significantly reduce costs or enhance experiences, especially if you travel frequently or make regular purchases in certain categories.

Consumer Protections

Credit cards also come with robust consumer protections. These include:

- Fraud Protection: If someone uses your card without permission, you’re typically not liable for unauthorized charges.

- Purchase Protection: Many cards cover damage or theft of new purchases within a specific time frame after buying them.

- Extended Warranties: Some credit card companies extend the manufacturer’s warranty on eligible items.

Such protections provide peace of mind, ensuring you’re safeguarded against potential losses and fraud while using your card.